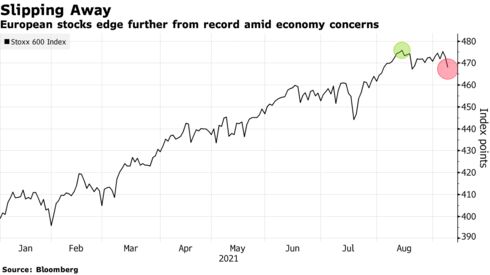

European shares dropped amid a blurred outlook for global growth, as investors await Thursday’s update from the European Central Bank. The Stoxx Europe 600 Index was down 1.1% as of 9:01 a.m. in London, trading at its lowest level since Aug. 19 as automakers, banks and industrials led losses. Miners and technology outperformed, but all sectors were lower. Volumes for Euro Stoxx 50 futures in the first hour of trading was double the 30-day average. Investment firm EQT AB fell 6.3% as an investor sold stock, part of a flurry of share sales on Tuesday that also included SoftwareOne Holding AG, automaker Stellantis NV and online retailer Asos Plc.

Europe’s main stock benchmark has struggled for traction after hitting an all-time high last month. While coronavirus vaccination programs are expected to continue to drive the economic reopening, disappointing economic data has distorted the recovery path just as interest rate-setters consider scaling back support. “A bit of a pull-back on the potentially slowing growth concerns is always likely,” Marija Veitmane, a multi-asset strategist at State Street Global Markets, said in written comments. The Delta Covid-19 variant has the potential to slow the global economic recovery, she added. Traders are now looking ahead to the European Central Bank’s policy update: “There will be a bit of sitting out, waiting to hear how much the ECB slows purchases,” Guy Foster, chief strategist at Brewin Dolphin, said in written comments. Some fund managers coming back from vacations may also be taking profits, Foster added. Governing Council member Robert Holzmann told Eurofi Magazine Wednesday that the ECB may normalize policy “sooner than most financial market experts expect.” The broader outlook for European equities is supported by the recent rebound in corporate profits, according to BlackRock. “Valuations remain attractive relative to history and look even more attractive than at the start of the year thanks to strong earnings,” strategists including Wei Li wrote in a report. Bankers’ views on global equities have turned slightly more negative, with firms including Morgan Stanley and Credit Suisse Group AG cautioning on the U.S. market. Both are more positive on Europe, however. Among individual shares, Sanofi slipped 1% after agreeing to buy immune-system therapies firm Kadmon Holdings Inc. for $1.9 billion. Airlines including EasyJet Plc and Ryanair Holdings Plc gained as the Telegraph newspaper reported that the U.K. may scrap its green and amber warning lists for foreign travel next month.